Agricultural Land Tax Rules in Karjat Explained

In This Article

Purchase or sale of agricultural land in Karjat is a massive choice. The majority of the population is concerned with the price, location, and potential development. However, there is one major variable that is easily ignored: tax regulations. The act of neglecting taxation may cause some unanticipated financial costs and legal issues in the future.

In Maharashtra, the rate of sale of agricultural land largely depends on its location and the time of holding the land. The sale can be of full exemption in certain cases. In other cases, there may be income tax on the sale of agricultural land or capital gains on the sale of agricultural land.

This is the reason why, before involving oneself in any transaction, it is important to learn the agricultural land tax regulations in Karjat. Whether you are buying land in Karjat for the first time, investing in property, or planning to sell inherited land, understanding the tax implications in advance can help you avoid unpleasant surprises and make informed decisions.

What Is Agricultural Land Under Income Tax Law?

Before understanding the sale of agricultural land taxability, it is important to know how agricultural land is defined under income tax laws.

The agricultural land under the Income Tax Act generally refers to land that is utilized in farming, such as cultivation, crop growing, or agricultural production. Not every piece of agricultural land, however, is applied identically to taxation. Location is the most important criterion to determine the taxability.

Rural Agricultural Land

The agricultural land in the rural areas is typically not considered a capital asset under the income tax law. This implies that in case such land is sold, there is no tax on capital gain on the sale of agricultural land.

The land is said to be rural when it falls outside designated municipal boundaries and when it is situated some distance away beyond urban boundaries. Essentially explained, the land located in truly rural regions is usually not subject to capital gains tax.

Urban Agricultural Land

Urban agricultural land is considered a capital asset. The capital gain on the sale of agricultural land is taxable when it is sold.

In case the agricultural land within the notified municipal limits or the prescribed distance of a municipality in Karjat falls under the jurisdiction of the tax on the sale of agricultural land, it becomes applicable. The seller can be required to pay short-term or long-term capital gains tax in other instances, depending on the holding period.

Why Location in Karjat Matters

Karjat has both rural and developing areas. Some parts may qualify as rural for tax purposes, while others may fall under urban classification due to proximity to municipal boundaries.

This classification directly impacts income tax on the sale of agricultural land. Therefore, before buying or selling, it is important to verify whether the land is treated as rural or urban under tax law.

Understanding this distinction is the first step in determining whether the sale will be tax-free or taxable.

What Determines Tax on Sale of Agricultural Land in Karjat?

When you sell agricultural land in Karjat, the tax is not decided randomly. It depends on clear rules under the Income Tax Act.

To understand the sale of agricultural land taxability, you must check three main things:

- Is the land treated as a capital asset?

- Is there a profit?

- Does any exemption apply?

Let us understand each point properly.

1. Is the Land Treated as a Capital Asset?

- Tax applies only if the land is treated as a capital asset under income tax law.

- A capital asset is any property that becomes taxable when sold for a profit.

- If agricultural land falls under the definition of a capital asset, then capital gain on the sale of agricultural land must be calculated.

Agricultural land is considered a capital asset when it falls under the definition given in Section 2(14) of the Income Tax Act, 1961.

Under this section:

- Rural agricultural land is not treated as a capital asset.

So, no capital gains tax applies to its sale. - Urban agricultural land is treated as a capital asset.

So, capital gain on the sale of agricultural land becomes taxable.

If it does not fall under this definition, then even if you sell it at a higher price, the capital gains tax on agricultural land sales will not apply.

2. Is There a Profit From the Sale?

Tax is charged only on profit, not on the total sale value.

Profit means = Sale Price – Purchase Price – Allowed Expenses

If the sale price is higher than the purchase price, there is a capital gain.

If there is no profit, there is no capital gain, and therefore no income tax on the sale of agricultural land.

So even if the land is taxable in nature, the tax applies only when there is a gain.

3. Does Any Exemption Apply?

Even if the land is treated as a capital asset and there is profit, tax may still be reduced or avoided through exemptions. An exemption means the law allows you not to pay tax if certain conditions are met.

One common exemption is under Section 54B of the Income Tax Act.

Under this section, if a person sells agricultural land and buys another agricultural land within the allowed time period, the capital gain tax may be reduced or fully exempt.

However, certain conditions must be satisfied, such as:

- The land should have been used for agricultural purposes

- The new land must be purchased within the specified time

If these conditions are not met, the exemption may not be allowed.

4. Holding Period Also Matters

If the land is taxable and no exemption applies, the next step is to check how long the land has been held.

The holding period decides whether the gain is:

- Short-term capital gain

- Long-term capital gain

This affects how much capital gains tax on agricultural land sales will be payable. Many people assume that agricultural land is always tax-free. This is not always correct.

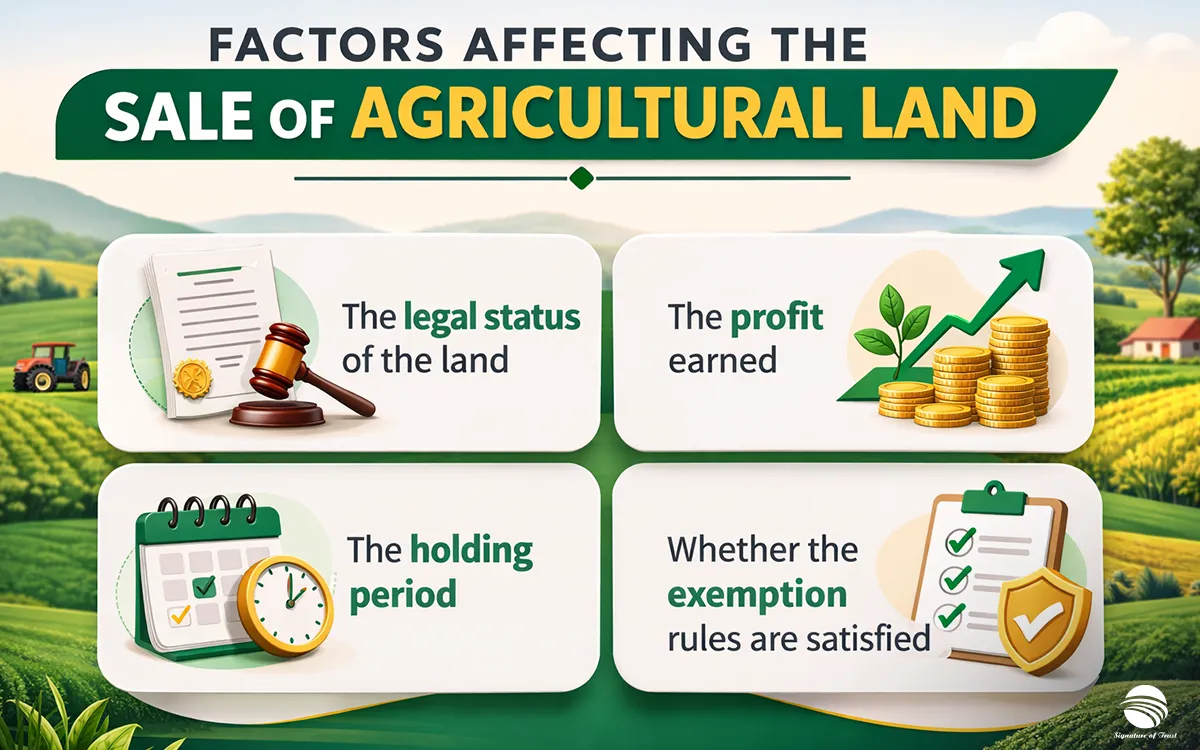

In Karjat, the income tax on agricultural land sales depends on:

- The legal status of the land

- The profit earned

- The holding period

- Whether the exemption rules are satisfied

Only after checking all these factors can the correct tax liability be determined. Understanding these rules before selling helps avoid unexpected tax notices, penalties, or last-minute financial stress.

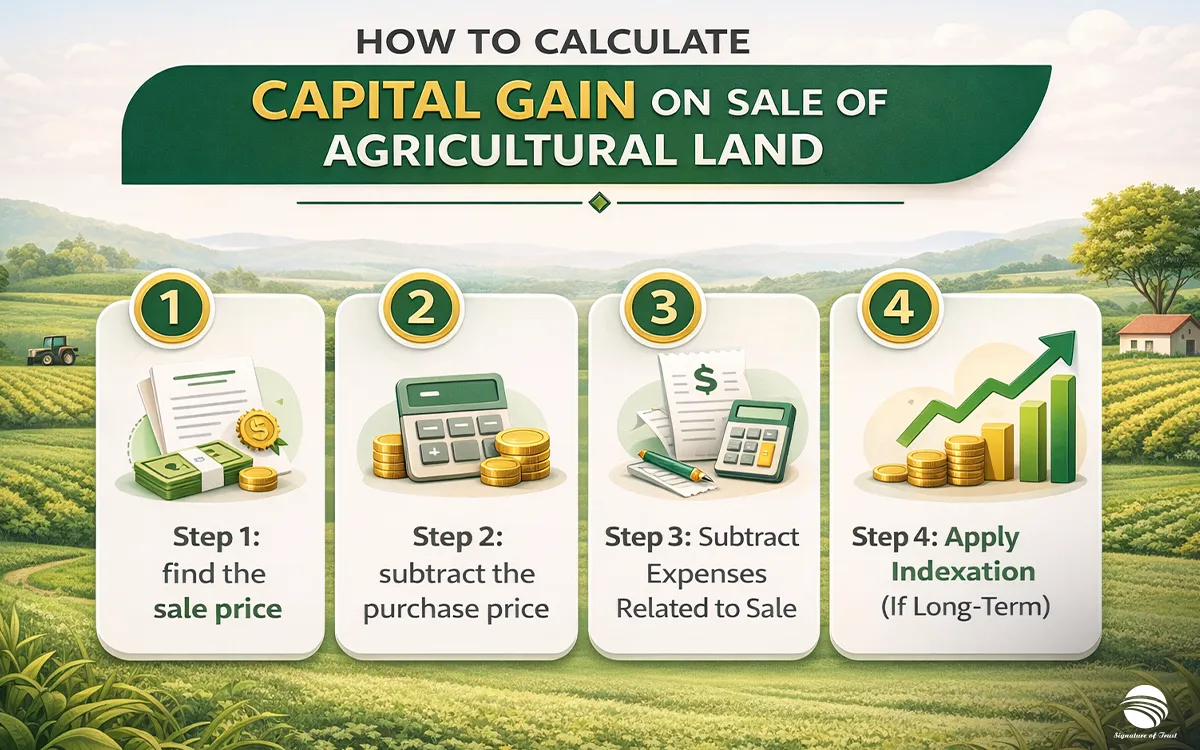

How to Calculate Capital Gain on Sale of Agricultural Land

If the sale of agricultural land in Karjat is taxable, the next step is to calculate the capital gain.

Remember, tax is charged only on the profit, not on the full sale amount.

Let us understand this step by step.

Step 1: Find the Sale Price

This is the amount you receive when you sell the land.

In some cases, stamp duty value may also be considered if it is higher than the actual sale price. This is as per the income tax rules.

Step 2: Subtract the Purchase Price

This is the amount you originally paid to buy the land.

If the land was inherited, the purchase price of the previous owner is considered.

Step 3: Subtract Expenses Related to Sale

You can also deduct certain expenses, such as:

- Brokerage

- Legal fees

- Stamp duty paid at the time of purchase

- Registration charges

These reduce the capital gain on the sale of agricultural land.

Step 4: Apply Indexation (If Long-Term)

If the land was held for more than 24 months and qualifies as long-term, you may get the benefit of indexation.

Indexation adjusts the purchase price for inflation. This reduces the taxable profit and lowers the capital gain tax on agricultural land sales.

Simple Example

Suppose:

- Purchase price: ₹10 lakh

- Sale price: ₹25 lakh

- Expenses: ₹1 lakh

Capital Gain = ₹25 lakh – ₹10 lakh – ₹1 lakh

= ₹14 lakh

If indexation applies, the taxable gain may be reduced further. Tax will then be calculated on the final gain amount.

Many people calculate tax only on the sale amount. This is incorrect.

Income tax on the sale of agricultural land is charged only on the net capital gain after deductions and benefits.

A proper calculation ensures correct tax payment, no penalty or notice, and better financial planning.

Short-Term and Long-Term Capital Gain on Agricultural Land

When the sale of agricultural land in Karjat is taxable, the holding period becomes very important. The number of months you owned the land decides whether the capital gain is short-term or long-term. This directly affects the income tax on the sale of agricultural land.

-

Short-Term Capital Gain (STCG)

If agricultural land is sold within 24 months from the date of purchase, the profit is treated as a short-term capital gain.

In this case, the gain is added to your total income for the year. It is taxed according to your income tax slab rate. This means the tax rate depends on how much total income you earn in that financial year.

If you fall under a higher tax bracket, the tax on the sale of agricultural land will also be higher. There is no indexation benefit available for short-term gain.

-

Long-Term Capital Gain (LTCG)

If agricultural land is held for more than 24 months before selling, the profit is treated as a long-term capital gain.

In this case, the seller usually gets the benefit of indexation. Indexation adjusts the original purchase cost to account for inflation. Because of this, the taxable capital gain on the sale of agricultural land becomes lower.

Long-term capital gain is taxed at a fixed rate as per income tax rules, which is generally lower than the short-term tax for many taxpayers.

Even a small difference in holding period can change the tax result. Selling land after 23 months and selling after 25 months can lead to different tax treatment.

For landowners in Karjat, checking the holding period before finalising the sale can help reduce capital gains tax on agricultural land sales and improve overall tax planning.

Key Scenarios for Income Tax on Agricultural Land Sale in India

The income tax on the sale of agricultural land does not apply in the same way in every case. The tax treatment can change depending on who is selling the land and how the land was acquired.

Let us look at some common situations.

1. Individual Seller

When an individual sells agricultural land, the tax depends on whether the land is treated as a capital asset and whether there is a profit.

If the land is taxable and there is a capital gain, the seller must pay tax based on whether the gain is short-term or long-term. The income tax on the sale of agricultural land will be calculated in the seller’s individual income tax return.

If exemption conditions are satisfied, tax may be reduced or avoided.

2. Joint Ownership

In many cases, agricultural land in Karjat is owned jointly by family members.

When jointly owned land is sold, the capital gain is divided among the co-owners according to their ownership share. Each owner must report their share of capital gain on their own income tax return.

Tax is calculated separately for each person. This means the tax liability may differ depending on each person’s income slab and exemptions available to them.

3. Inherited Agricultural Land

If agricultural land is inherited, tax rules are slightly different.

Capital gain is calculated using the original purchase price paid by the previous owner. The holding period of the previous owner is also counted while determining whether the gain is short-term or long-term.

Income tax on the sale of agricultural land in inherited cases applies only when the land is sold, not when it is inherited.

Inheritance itself does not attract tax. Tax arises only at the time of sale.

4. Converted Agricultural Land

Sometimes, agricultural land is converted into non-agricultural (NA) land before sale.

Once converted, the tax treatment may change. The land may clearly fall under the definition of a capital asset. In such cases, capital gain on the sale of agricultural land becomes taxable.

The date of conversion and the date of sale both become important for calculating tax.

5. Agricultural Land Sold to Developers

In growing areas like Karjat, land is often sold to developers for projects.

Even if the buyer is a developer, the tax treatment depends on the classification of the land and the profit earned.

If the land is taxable, capital gains tax on agricultural land sale will apply in the normal way. In some cases, advance payments, agreements, or joint development arrangements may also have separate tax implications.

The income tax on the sale of agricultural land is not the same in every situation. Ownership type, method of acquisition, and land status all affect tax liability.

Before selling agricultural land in Karjat, it is important to review your specific situation. A small difference in ownership or land status can change the final tax amount.

Tax Exemptions Available on Agricultural Land Sale

Even if a capital gain arises on the sale of agricultural land, the Income Tax Act allows certain exemptions. These exemptions can reduce or fully eliminate the income tax on the sale of agricultural land if specific conditions are satisfied.

The most important exemption for agricultural land is under Section 54B.

Section 54B Exemption

Section 54B provides relief when an individual or a Hindu Undivided Family (HUF) sells agricultural land and reinvests the sale amount in another agricultural land.

If the conditions are met, the capital gain on the sale of agricultural land can be reduced by the amount invested in the new land. If the entire capital gain is reinvested, the tax may become zero.

This exemption applies only when the land sold was used for agricultural purposes.

Reinvestment Conditions and Time Limits

To claim this exemption, the agricultural land sold must have been used for farming for at least two years before the sale.

The seller must purchase another agricultural land within two years after the date of sale. In some cases, a purchase made up to one year before the sale may also qualify.

If the amount is not immediately invested before filing the income tax return, it should be deposited in the Capital Gains Account Scheme. If the reinvestment is not completed within the allowed time, the exemption will not be available.

Documentation and Common Mistakes

Proper records are important when claiming an exemption. The seller should maintain proof that the land was used for agricultural purposes, along with the sale and purchase documents.

Common reasons for rejection include:

- Failure to prove agricultural use

- Missing the two-year purchase deadline

- Investing in non-agricultural property

- Not depositing unused funds in the required scheme

Even small mistakes can result in full capital gain tax on agricultural land sale becoming payable.

For landowners in Karjat, Section 54B can significantly reduce tax liability. However, the benefit is available only when all conditions are carefully followed and properly documented.

Important Tax Considerations for Agricultural Land Buyers in Karjat

When buying agricultural land in Karjat, most buyers focus only on price and location. However, it is equally important to understand the tax and legal aspects connected to the sale of agricultural land. A small mistake at the time of purchase can lead to financial or legal problems later.

Below are some important points every buyer should consider.

1. Stamp Duty vs Income Tax - Know the Difference

Stamp duty and income tax are two different things. Stamp duty is paid by the buyer at the time of registration of the property. It is calculated on the agreement value or the government ready reckoner value, whichever is higher.

Income tax on the sale of agricultural land, on the other hand, is generally the responsibility of the seller. It is charged on the capital gain earned from the transaction.

However, buyers should still understand the tax on the sale of agricultural land because:

- If the sale value is lower than the stamp duty value, tax implications may arise.

- The declared transaction value must be accurate and properly recorded.

Understanding this difference helps avoid confusion between registration cost and tax liability.

2. TDS Implications (Tax Deducted at Source)

In certain cases, the buyer may be required to deduct TDS before paying the seller. If the agricultural land is treated as a capital asset and the transaction value exceeds the prescribed limit under income tax rules, TDS provisions may apply.

This means:

- The buyer must deduct a small percentage of the sale value.

- The deducted amount must be deposited with the government.

- The balance amount is paid to the seller.

Failure to deduct TDS when required can result in a penalty and interest for the buyer. Therefore, checking whether TDS applies to the sale of agricultural land is very important before making a payment.

3. Due Diligence Before Buying Agricultural Land

Before purchasing agricultural land in Karjat, proper verification is essential.

A buyer should:

- Confirm whether the land is legally classified as agricultural.

- Verify clear title and ownership.

- Check whether the land falls under taxable classification.

- Review past usage records to ensure it qualifies as agricultural land.

This protects the buyer from future disputes and unexpected tax issues.

4. Conversion to Non-Agricultural (NA) Land and Tax Impact

In developing areas of Karjat, buyers often purchase agricultural land with plans to convert it into non-agricultural (NA) land for construction or development. Once land is converted, its tax treatment can change. Future sale of converted land may attract different capital gains rules.

Buyers should understand:

- The legal process of conversion.

- Additional charges are involved.

- How the future tax on the sale of agricultural land may change after conversion.

Proper planning at the purchase stage helps avoid a higher tax burden later.

Even though income tax on the sale of agricultural land is mainly paid by the seller, buyers are not completely free from responsibility. Compliance with stamp duty rules, TDS provisions, and proper verification is necessary for a safe and legally sound transaction.

In fast-growing regions like Karjat, careful review before purchase ensures long-term financial security.

Plan Smart Before You Buy or Sell

Agricultural land transactions in Karjat involve more than agreeing on a price. The agricultural land tax rules in Karjat, the capital gain on the sale of agricultural land, and the eligibility for exemptions all play a major role in the outcome of the deal. Whether you are buying or selling, understanding the tax on the sale of agricultural land in advance helps you avoid unexpected costs and future complications.

Proper verification of land classification, ownership structure, holding period, and documentation ensures that the income tax on the sale of agricultural land is correctly assessed. A well-informed decision today can prevent legal issues or financial stress later.

In this process, local knowledge makes a difference. Universal Properties Karjat supports buyers and sellers by guiding them through documentation checks, transaction procedures, and practical due diligence. With the right guidance and clarity at every step, agricultural land transactions can be handled smoothly, confidently, and in full compliance with the law. Contact us to get expert assistance and make the entire process simple and hassle free.

FAQs (Frequently Asked Questions)

Income tax on the sale of agricultural land in Karjat depends on whether the land is treated as a capital asset under the Income Tax Act. If the land is taxable and sold at a profit, capital gain tax will apply. If it does not qualify as a capital asset or meets exemption conditions, tax may not be payable. The holding period and profit amount also affect tax liability.

Capital gain on the sale of agricultural land is calculated by subtracting the purchase price and eligible expenses from the sale price. If the land is held for more than 24 months, the indexation benefit may apply to reduce the taxable gain. Tax is charged only on the net profit, not on the full sale amount.

Yes, you can claim exemption under Section 54B if you are an individual or HUF and you reinvest the capital gain in another agricultural land within the prescribed time limit. The land sold must have been used for agricultural purposes for at least two years before sale. If all conditions are met, the capital gain tax on agricultural land sale can be reduced or eliminated.

TDS on sale of agricultural land may apply if the land is treated as a capital asset and the transaction value crosses the prescribed limit under income tax rules. In such cases, the buyer may be required to deduct TDS before paying the seller. If the land does not qualify as a taxable capital asset, TDS provisions may not apply.

When agricultural land is converted into non-agricultural (NA) land, its tax treatment can change. Upon future sale, it is more likely to be treated as a capital asset, and capital gain tax may apply. The timing of conversion and sale plays an important role in calculating income tax on sale of agricultural land.